The International Faculty and Scholar Advisor advises departments on GMU and United States Citizenship and Immigration Services (USCIS) policies and procedures for employing foreign nationals to ensure compliance with U.S. immigration laws and regulations. In addition, the International Faculty Advisor prepares and files employment-based visa petitions with USCIS on behalf of George Mason University.

Employment

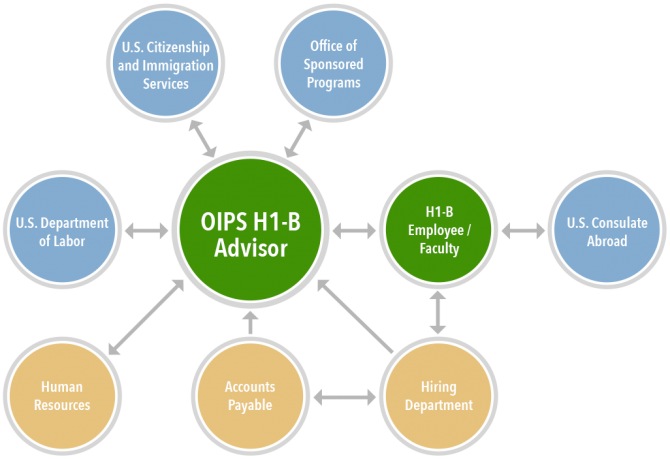

A few different offices on campus will help you with Onboarding: OIPS, the International Tax Office, and Central HR. See the Fiscal Services Hiring Guidance for Step by Step instructions on the steps you need to follow with OIPS, the Social Security office, and International Tax to finalize your on-campus work authorization.

1. Apply for SSN: For Social Security Administration you will need: passport, visa, signed contract, I-94 and SS-5 Form. Explore the links below:

- Social Security Administration Office

2. Complete MasonOnBoarding (the hiring department will send login information)

3. Complete I-9 Form with the International Tax Office.

4. Send H-1B Check-In Form and H-1B Agreement to [email protected].

Noelle Deola

Associate Director for International Employees and Exchange Visitors

Office of International Programs & Services

Student Union Building I Addition, 4th Floor, Suite 4300

Phone: (703)-993-2970

Fax: (703) 993-2966

Email: [email protected]

Mailing Address:

George Mason University

4400 University Drive, MSN 4C3

Fairfax, VA 22030 USA

Other Compensation

Independent contractors, e.g. guest lecturers, short-term research collaborators, etc. receiving non-employee compensation (honorarium)

- Departments should contact OIPS well in advance of arrival to discuss length of activity, appropriate immigration status, and what can or cannot be paid.

- Payees must arrange an appointment to meet with the Tax Coordinator. They will need to bring immigration documents to Human Recouses for verification of status.

- Do not need to complete an I-9 form

- May not qualify for an SSN. Treaty-eligible payees will need to apply for Individual Taxpayer Identification Number (ITIN), using IRS form W-7, if no SSN available. If not treaty-eligible, must apply for ITIN when they file U.S. tax return the following year.

- Complete Foreign National Information Form in OIPS.

- If eligible, complete form 8233 for tax treaty benefits

- If payment is for a visitor in B-1 (visitor for business), B-2 (visitor for tourism), VWB or VWT (waiver for business or tourism), a statement must be executed and signed by the visitor, attesting that their independent services at GMU did not exceed 9 days and that they have not received more than 5 similar payments from U.S. institutions in the prior six months.

- Department sends documents requesting payment, along with completed Employee/Independent Contractor Evaluation Form, to Tax Coordinator for verification and signature. Request will be forwarded to Sponsored Programs or Accounts Payable as appropriate.

New proposed USCIS rules require that an individual who enters the U.S. with the intention of receiving an honorarium or expense reimbursement enter the U.S. in business status (B-1 or VWB). Individuals who enter the U.S. in tourist status (B-2 or VWT) can only receive such payments if the income-providing opportunity arises AFTER they have entered the U.S. We suggest that ALL short-term visitors request to be admitted in business status to avoid complications.

Expense Reimbursement

Reimbursements of travel expenses for travel to GMU to participate in an academic or business function.

Payments are generally not reportable or taxable if properly documented and accounted for in accordance with GMU’s travel policy, and if expenses are incurred while conducting business on behalf of GMU. For travel grants for students or conference participants, see “Students Receiving Scholarship, Fellowship, or Award”

Procedure –

- Departments should contact OIPS well in advance of arrival to discuss length of activity, appropriate immigration status, and what can or cannot be paid.

- If feasible, arrange an appointment to meet with the Tax Coordinator. They will need to bring immigration documents for verification of status. In cases of reimbursement only, it may be possible to skip the tax appointment if department is willing to collect certain documents and copies of immigration documents. This can be discussed with the Tax Coordinator during initial contact in item 1 above.

- If payee is in the U.S. as a student or employee at another university or organization, they need to complete Foreign National Information Form and meet with Tax Coordinator.

- If payment is for a visitor in B-1 (visitor for business), B-2 (visitor for tourism), VWB or VWT (waiver for business or tourism) status, a statement must be executed and signed by the visitor, attesting that their independent services at GMU did not exceed 9 days and that they have not received more than 5 similar payments from U.S. institutions in the prior six months. Individuals in B-1 or VWB status whose activities exceed 9 days but are still eligible for expense reimbursements must sign a statement attesting that their stay in the U.S. will not exceed 12 months. Remember that B-2 or VWT individuals over 9 days are not eligible for ANY payments related to services rendered.

- Department sends documents requesting and substantiating expense reimbursement along with substantiation to Tax Coordinator for verification and signature. Request will be forwarded to Sponsored Programs, Travel or Accounts Payable as appropriate.

- Those on B-1/B-2/WB/WT visa may receive reimbursement of travel expenses in lieu of honoraria (less paperwork and faster, but must provide travel receipts. B-2 and WT visitors are subject to time and frequency restrictions mentioned previously.)

Do’s and Don’ts Primer for Payments to Foreign Nationals

DO contact Human Resources with questions regarding the appropriate immigration status, payment possibilities, acceptable duration of activity, etc. for anyone to whom you wish to make a payment before you make any promises.

DON’T promise payment or employment to someone without making it contingent upon their acquiring an immigration status that allows them to receive the payment from or be employed by GMU. For example, a J-1 researcher on Villanova’s DS-2019 is NOT automatically eligible to receive an honorarium for lecturing at GMU.

DO be certain to properly classify the type of income you pay someone. A fellowship, for example, is non-compensatory by definition. If you require services in return for a payment or other financial benefit (i.e. tuition waiver), it is not a fellowship; it is compensation and must be paid, taxed, and reported as such.

DON’T complete I-9s, W-4s or state withholding documents in the department. These must be done in Human Resources New Employees Center.

DO carefully consider how you assign job codes. Each job code has inherent assumptions that affect our employees (i.e., an adjunct is always FICA taxed, whereas a “student worker” may only be FICA taxed during the summer).

DON’T let the bureaucracy put you off – we are here to help both you and our international visitors, but complying with regulations is the only way we can do our jobs well.